Retirement Income Planning for Bay Area Retirees

Turn $1M+ in retirement savings into a tax-efficient income that lasts.

Fee-only fiduciary planning for Bay Area pre-retirees and retirees, built around proprietary withdrawal-tax optimization software.

The first five years of retirement decide the next thirty.

For Bay Area households with $1 million or more in retirement savings, the transition from accumulating to drawing down is the most consequential financial decision of your life — and the one where most retirees receive the least useful guidance. Decisions made in the first five years of retirement compound across every year that follows. Get them right and you protect three decades of cash flow, taxes, and legacy. Get them wrong and the cost is six or seven figures over a 30-year retirement.

Living in the Bay Area amplifies every variable. Cost of living runs roughly twice the national average. California state income tax stacks on top of federal. Concentrated equity from technology employers creates outsized capital gains exposure. Property values mean estate planning isn't optional. None of this is handled well by retirement rules of thumb developed for the national median household.

Index Gurus, Inc. is a fee-only fiduciary registered investment adviser based in Concord, California. We work directly with pre-retirees and retirees in the Bay Area to build retirement income plans that start with your objectives and risk tolerance, then design a tax-aware income strategy around them.

Foundation first: a Retirement Lifestyle Plan built on your goals.

Every Index Gurus retirement income plan starts with the same premise: the right strategy depends on who you are, not on a default formula. Two households with identical balance sheets can have completely different optimal plans because their objectives, time horizons, and tolerance for risk are different. Skipping this step — which most retirement calculators and many advisors do — is the single biggest reason plans fail in practice even when the math works on paper.

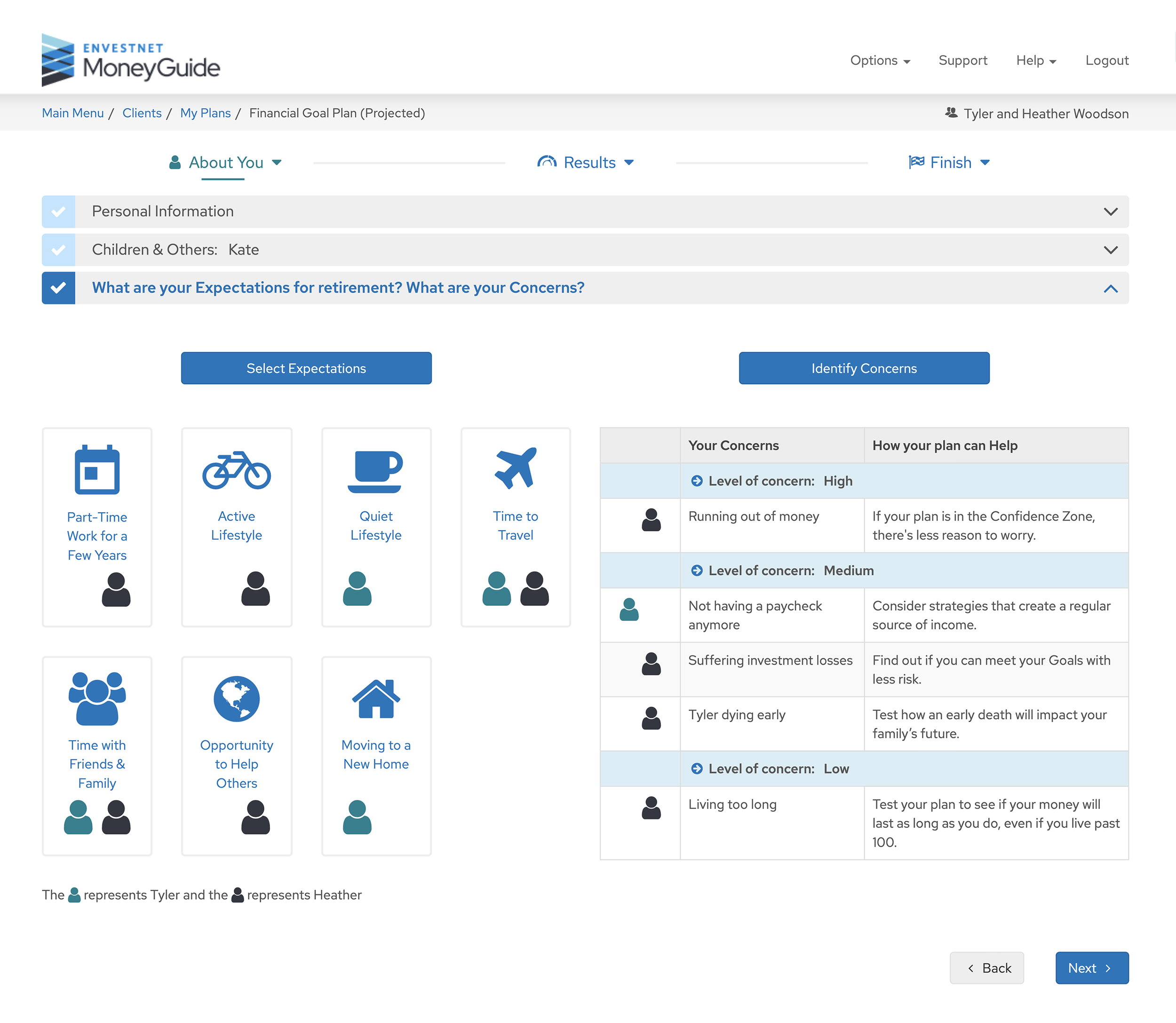

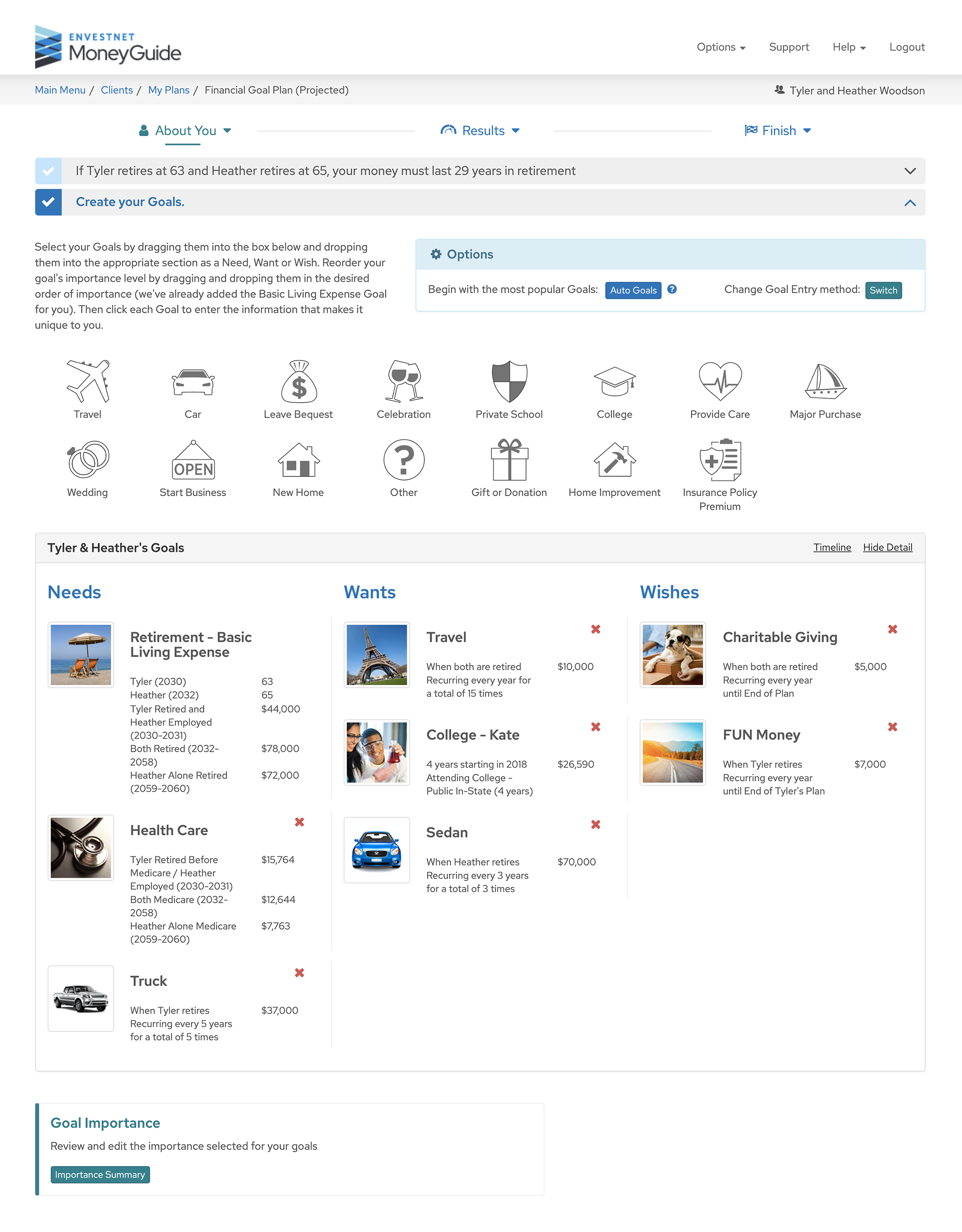

Before we discuss any specific tax tactic or withdrawal strategy, we establish your foundation using a structured framework: your Needs, your Wants, and your Wishes.

Must-have goals

The expenses that fund the retirement you require — non-negotiable, regardless of market conditions.

- Basic living expenses

- Health care and Medicare premiums

- Housing, transportation, utilities

- Long-term care contingency

Would-like-to-have

The expenses that make retirement meaningful — important but adjustable if circumstances change.

- Annual travel and experiences

- Vehicle replacements

- Home improvement

- Hobbies and recreation

Dream-of goals

The aspirational goals — wonderful to fund if the plan supports them, acceptable to scale back if not.

- Gifts to children and grandchildren

- Charitable giving and legacy bequests

- Second-home purchase

- Major celebrations

This goals hierarchy is the anchor of your entire plan. Every downstream decision — from asset allocation to withdrawal sequencing to Social Security claiming — is evaluated against whether it protects your Needs, supports your Wants, and gives your Wishes a realistic chance.

How we build your Retirement Lifestyle Plan.

Six steps, in this order, following our planning approach. Each builds on the previous one. We do not skip ahead.

Goals

Identify all your goals and rank their importance — Needs, Wants, and Wishes.

Resources

Inventory what funds those goals — income sources, investments, savings, other assets.

Risk and Return

Determine the balance of risk and return that is right for you — both emotionally and analytically.

Review and Discuss

Review where you are today and what it takes to reach your Confidence Zone.

Plan

Create your written Retirement Lifestyle Plan — the document you reference annually thereafter.

Implement

Execute the savings strategy, asset allocation, and tactical decisions the plan calls for.

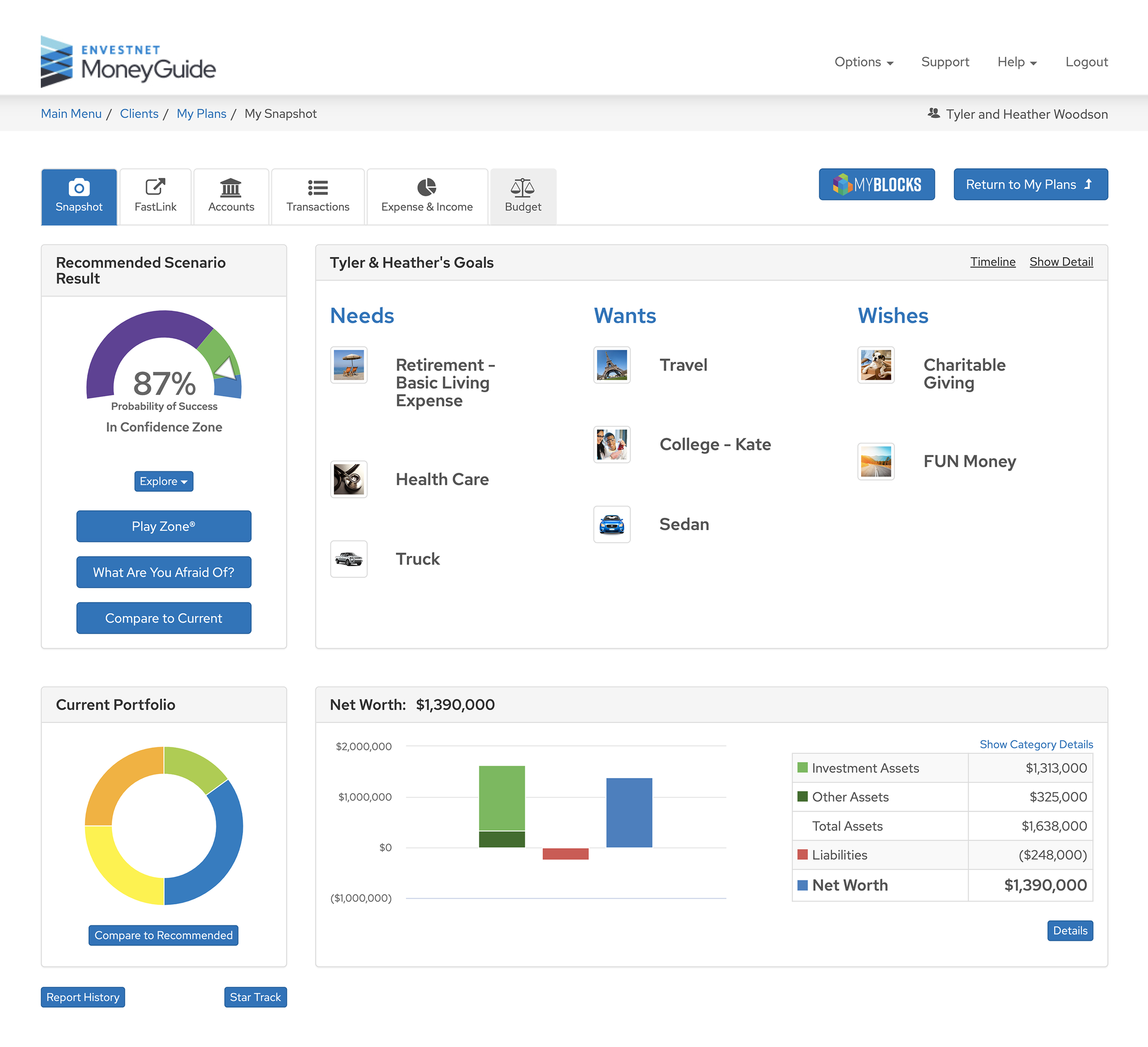

A 70%–90% probability of funding your goals.

We design every Retirement Lifestyle Plan to land inside the Confidence Zone — a Monte Carlo probability-of-success range typically between 70% and 90%, calibrated to your age and circumstances. Above 90% may mean you are giving up more in lifestyle today than is necessary. Below 70% leaves too much uncertainty for the years ahead.

The Confidence Zone is the right balance between living well today and protecting against future shocks. It is the metric that guides every recommendation we make.

The decisions that shape lifetime retirement outcomes.

Once we understand your foundation, a complete retirement income strategy addresses six interconnected decisions. Each interacts with the others; none can be optimized in isolation.

Withdrawal sequencing

The order in which you draw from taxable, tax-deferred, and tax-free accounts shapes your lifetime tax bill more than almost any other decision. Conventional wisdom (taxable first, then tax-deferred, then Roth) is often suboptimal for $1M+ households.

Tax-efficient income mix

For each year of retirement, what is the right blend of withdrawals from each account type to maximize after-tax cash flow while staying out of higher tax brackets and IRMAA tiers? This is where DrawDownIQ does its most concentrated work.

Social Security claiming

The decision to claim at 62, full retirement age, or 70 has implications across longevity, taxation, spousal and survivor benefits, and household withdrawal timing. "Wait until 70" is not always right.

IRMAA bracket management

For 2026, Medicare IRMAA surcharges begin at $218,000 MAGI for joint filers. The cliff structure means a single dollar over a threshold can cost a couple thousands per year in additional Medicare premiums — for two years.

Sequence-of-returns risk

The order in which investment returns occur during the withdrawal phase affects portfolio survival more than the average return itself. A poor first decade can permanently impair a plan that would have worked under any reasonable long-run assumption.

RMD planning

Required Minimum Distributions begin at age 73 and rise as a percentage of account balances every year thereafter. Without advance planning, RMDs frequently push retirees into permanently higher tax brackets and IRMAA tiers in their late 70s and 80s.

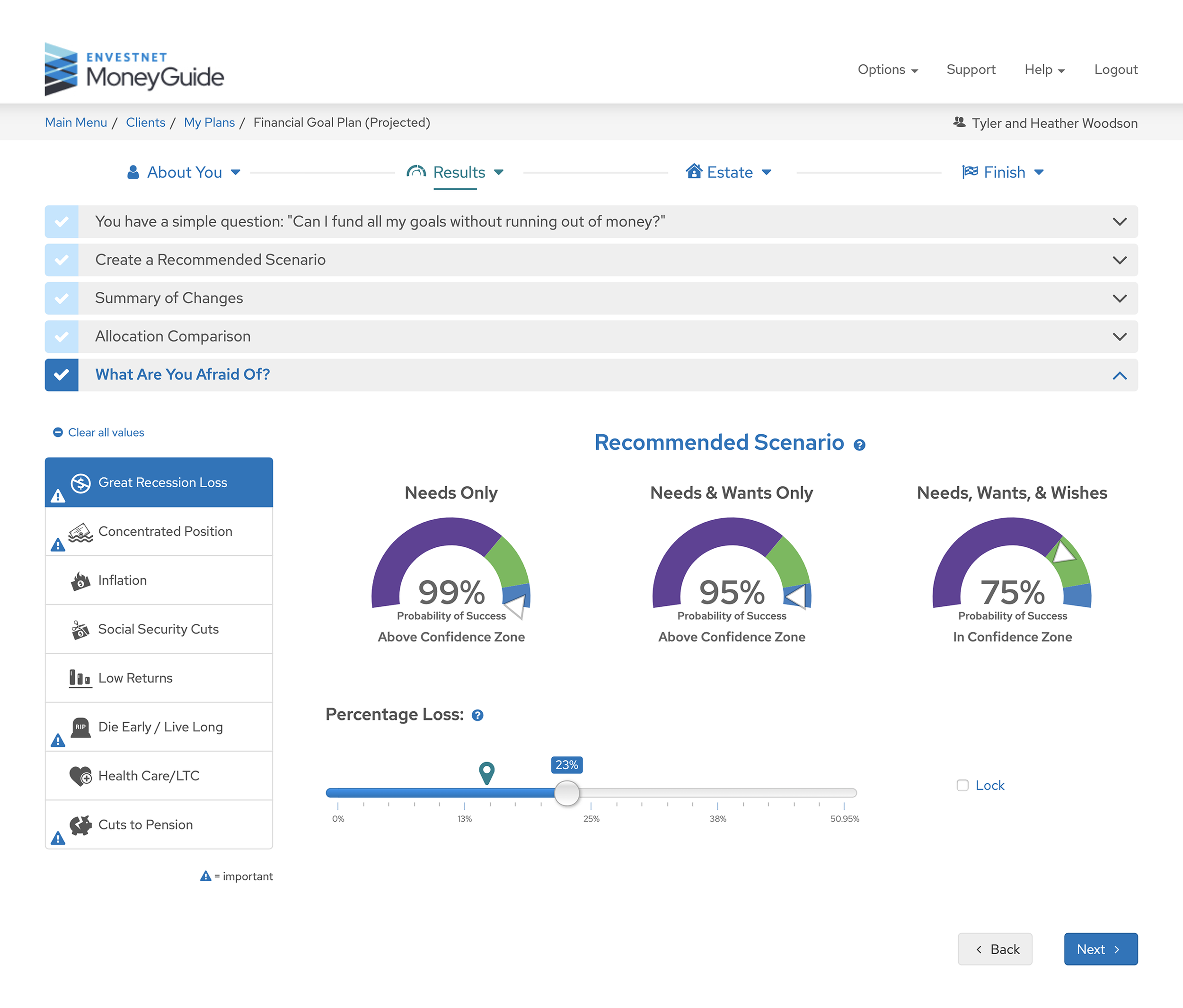

What if everything goes wrong at once?

A plan that works in average conditions is not a plan. We stress-test every Retirement Lifestyle Plan against the specific shocks that historically have derailed retirees — and we tell you, in concrete probability terms, how your plan holds up against each one.

We model your plan against each of these scenarios as part of the foundation phase:

The output of this stress testing directly informs your asset allocation, your cash reserve strategy, and the Confidence Zone target we plan toward. If a scenario reveals that your Wishes are too aggressive given your risk tolerance, we say so. If your plan is more resilient than you thought, we tell you that too.

What separates our process: the foundation, the framework, and the math.

Most Bay Area advisors deliver one half of a retirement income solution: either a financial plan written without the analytical depth to model tax outcomes, or a software-generated projection that ignores the qualitative half of a real household's life. We deliver both, and we built our own software to do it.

Holistic Retirement Plan

A written, comprehensive plan built around your Needs, Wants, and Wishes — the framework that anchors every analytical decision. Each engagement covers:

- Needs, Wants, and Wishes — your goals hierarchy

- Resources inventory across all income and asset sources

- Risk and return calibration to your Confidence Zone

- Withdrawal sequencing and tax-efficient income mix

- Social Security claiming, with spousal and survivor analysis

- IRMAA bracket management for the current and upcoming year

- Investment allocation and risk management

- Estate, beneficiary, and charitable giving coordination

- Insurance and long-term care considerations

- Coordination with your CPA and estate attorney

DrawDownIQ — current-year tax optimization

Software we built in-house to answer one of the highest-stakes annual questions in retirement: what is the best withdrawal mix for this year, given current taxes, IRMAA thresholds, and RMD requirements? Every DrawDownIQ analysis produces:

- Three competing withdrawal strategies, side by side

- Marginal bracket and effective tax rate for each strategy

- Estimated federal tax and California state tax for each

- Current-year IRMAA exposure analysis

- Specific dollar recommendations across IRA, Roth, and brokerage draws

- A recommended action plan with concrete next steps

Neither component alone is sufficient. A plan without rigorous tax math makes recommendations the numbers don't support. Software output without a financial plan around it is just a calculation in search of a context. The combination — foundation first, framework second, math third — is what produces decisions you can act on with confidence.

Three competing strategies, side by side — for this year.

The most useful question DrawDownIQ answers is also the one most retirees never get a clear answer to: given what I have today, which withdrawal strategy produces the best after-tax outcome for the current year?

Every retirement income plan we deliver includes a side-by-side comparison of three withdrawal strategies for the current tax year. The same household, the same starting balances, the same Social Security election — three different ways to fund this year's income. The output makes visible what is otherwise invisible: which strategy delivers the most after-tax cash flow, which keeps you under IRMAA thresholds, which fills bracket headroom most efficiently, and which produces the smallest current-year tax bill.

Tax-smart blend

A coordinated draw from each account type this year, sized to fill specific tax brackets without crossing IRMAA thresholds. Often the most tax-efficient strategy for households with meaningful balances across all account types.

IRA-first

Draw primarily from tax-deferred accounts this year, accepting higher current taxes in exchange for reducing future RMD exposure. Used selectively in years where future bracket reduction outweighs current tax cost.

Strategic 4% withdrawal

A measured 4% withdrawal rate this year, drawing predominantly from taxable accounts and minimizing tax-deferred distributions. Preserves longevity of tax-deferred balances while maintaining a stable income floor.

The right strategy for this year depends on your foundation — your objectives, your goals, and your risk tolerance, the same foundation that anchors our comprehensive financial planning for high-net-worth households — applied to the specific tax environment of the current year. The strategy we recommend is the one that holds up against the realistic range of outcomes your household might experience this year, not the one that wins narrowly under the most optimistic assumption.

This is the answer to the question every retiree quietly carries: am I making the right withdrawal decisions this year? DrawDownIQ makes those decisions, and their consequences, visible.

Request a free promo code.

DrawDownIQ is a paid subscription tool that lets you analyze your retirement withdrawal options for the current tax year — comparing strategies across federal taxes, IRMAA thresholds, and Required Minimum Distributions. To explore it before deciding whether to subscribe, request a free promo code. Click the button below and your email will open with the request pre-filled — send it and we will reply with a code within one business day.

Email me a promo codeDrawDownIQ outputs are educational and illustrative; they do not constitute personalized financial, tax, or legal advice. Promo codes are issued by Index Gurus, Inc.

How an engagement works.

Discovery call

A 30-minute conversation, at no cost, to understand your situation, your most pressing decisions, and what you want from a long-term advisor relationship. By the end of the call we will tell you honestly whether the engagement is a fit.

Financial planning engagement

Standalone planning engagements start at $2,950 and produce a written plan covering objectives and risk-tolerance foundation, withdrawal sequencing, Social Security, IRMAA, investments, estate, and insurance — typically delivered in four weeks across three working sessions.

Ongoing relationship

Households with $1 million or more in investable assets may engage Index Gurus for ongoing investment management and continued planning, billed as an annual percentage of assets under management.

Frequently asked questions.

What is retirement income planning?

Retirement income planning is the process of converting accumulated savings across taxable, tax-deferred, and tax-free accounts into a sustainable, tax-efficient income stream that supports a retiree's desired lifestyle. It addresses withdrawal sequencing, Social Security claiming, Roth conversions, sequence-of-returns risk, RMDs, and IRMAA exposure as a coordinated whole.

How is retirement income planning different from investment management?

Investment management focuses on portfolio construction and ongoing oversight. Retirement income planning addresses how money flows out of the portfolio: in what order, from which accounts, with what tax consequences, coordinated with Social Security, pensions, RMDs, and other income sources. The two complement each other; a good plan requires both.

What is the Confidence Zone?

The Confidence Zone is a probability-of-success range — typically between 70% and 90% — that represents a healthy balance between current lifestyle and protection against future shocks. Every Retirement Lifestyle Plan we deliver is designed to land within this range, calibrated to your age and circumstances. A plan above 90% may mean you are sacrificing more lifestyle today than necessary. A plan below 70% leaves too much uncertainty. The Confidence Zone is the metric that guides every recommendation we make.

What is DrawDownIQ?

DrawDownIQ is proprietary retirement-distribution tax-optimization software developed by Index Gurus. It analyzes the best withdrawal strategy for the current tax year across federal taxes, IRMAA surcharge tiers, and Required Minimum Distributions. Every comprehensive retirement income plan we deliver includes specific DrawDownIQ analysis. A free promo code is available on request to try the tool yourself before subscribing.

When should I start retirement income planning?

Most planning value is created in the years leading up to and immediately following retirement — typically the period between age 60 and the start of Required Minimum Distributions at age 73. Decisions made during this window often shape outcomes for the next 20 to 30 years. Earlier engagement allows more time to align your portfolio with your objectives and risk tolerance, manage concentrated positions, and build flexibility into your Social Security claiming decisions.

What is withdrawal sequencing?

Withdrawal sequencing is the strategic order in which a retiree draws from taxable, tax-deferred, and tax-free accounts to fund retirement spending. The conventional rule of "taxable first, then tax-deferred, then Roth" is often suboptimal for $1M+ households because it ignores tax-bracket management, IRMAA thresholds, and the long-term consequences of tax-deferred balance growth on future RMDs.

Do you help with Social Security claiming decisions?

Yes. Social Security claiming optimization is a standard component of every retirement income plan. The decision to claim at 62, full retirement age, or 70 — and the spousal and survivor benefit interactions for couples — is evaluated in the context of the household's full income picture, expected longevity, and tax exposure. We model multiple claiming strategies side by side rather than relying on rules of thumb.

What is the asset minimum to work with Index Gurus?

Standalone financial planning engagements are available without an asset minimum, with fees starting at $2,950. Ongoing investment management engagements are available to households with $1 million or more in investable assets.

Are you a fiduciary?

Yes. Index Gurus, Inc. is a registered investment adviser and operates as a fiduciary at all times, on all accounts, in all aspects of the client relationship. We accept no commissions, referral fees, or third-party compensation. Our only revenue is the fee our clients pay us. Form ADV Part 2A is publicly available and we recommend reviewing it before any engagement.

Where is your office and do you meet remotely?

Our office is at 5350 Paso Del Rio Way, Concord, CA 94521. We meet clients in person at our office, at their preferred location in the East Bay or San Francisco, or via secure video conference depending on preference. We work with households across the entire Bay Area including Walnut Creek, Lafayette, Orinda, Danville, San Francisco, and the Peninsula.

Ready to talk?

Schedule a complimentary 30-minute discovery call. We will listen, ask focused questions, and tell you honestly whether the engagement is a fit. No sales pressure, no obligation.

Index Gurus, Inc. is a registered investment adviser. Information on this page is educational and does not constitute personalized financial, tax, or legal advice. Tax laws and IRMAA brackets referenced reflect rules in effect as of publication and are subject to change. Hypothetical examples and modeled scenarios are for illustrative purposes only; individual results vary. DrawDownIQ outputs are educational and illustrative; they do not constitute personalized advice. Please review Form ADV Part 2A for additional information regarding services, fees, and conflicts of interest. Past performance is not indicative of future results.

CFP Board owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER® in the U.S.